Quick summary: Biochar Carbon Credits Market explained: learn how biochar carbon credits are generated, verified, traded, and monetized, who benefits from biochar projects, key market standards, buyer considerations, and the role of traceability and dMRV in ensuring credit integrity.

A Comprehensive Buyer’s Guide to Understanding How They Work and Who Benefits

The biochar carbon credits market is experiencing unprecedented growth, with global market value reaching USD 235 million in 2024 and projected to grow at a CAGR of 27.4% to reach USD 2.14 billion by 2033. Biochar carbon removal credits represent one of the most tangible and scalable climate solutions available today, offering corporations, ESG funds, and climate-focused investors a high-integrity pathway to achieve net-zero targets. This comprehensive guide explores the mechanics of biochar carbon credits, verification standards, pricing dynamics, and strategic opportunities for buyers.

| 89% of 2025 biochar carbon credits are already committed to offtake agreements, signaling extreme scarcity and strong demand momentum from Fortune 500 companies. |

Biochar is a carbon-rich material produced through the pyrolysis of biomass a process that heats organic material (agricultural residues, forest waste, forestry byproducts) in the absence of oxygen. Unlike traditional burning, pyrolysis preserves carbon in a stable form that can persist in soil for hundreds to thousands of years.

One biochar carbon credit (1 BCR) represents one tonne of CO₂ equivalent permanently sequestered. When biochar is produced and applied to soil, the locked-in carbon is prevented from entering the atmosphere, creating a measurable and verifiable climate benefit.

Discover how biochar interacts with soil ecosystems, the science behind its benefits, and why it is becoming an important tool in climate-smart agriculture and land restoration strategies.

Read the full blog on Biochar and Soil Health →

| Metric | 2024 Value | 2033 Projection |

|---|---|---|

| Market Size (Global Biochar Credits) | $235 million | $2.14 billion |

| CAGR | — | 27.4% |

| Contracted Volume (since 2022) | — | 3.0+ million tonnes |

| Delivered (H1 2025) | — | 683,000 tonnes (22% delivery ratio) |

| 2025 Credits Committed | 89% | (up from 62% in March) |

North America: USD 82 million in 2024, growing at 25.8% CAGR. Driven by regulatory support, corporate net-zero commitments, and strong participation from Fortune 500 companies (Microsoft, Google, JPMorgan Chase).

Europe: USD 68 million in 2024. Leadership in climate policy, sustainable agriculture initiatives, and the recent EU Carbon Removals & Carbon Farming (CRCF) Regulation formally recognizing biochar as a permanent carbon removal solution.

Emerging Markets: India, Southeast Asia, and Latin America showing strong growth potential due to abundant biomass resources and agricultural focus. Samunnati’s Carbon Incubator Facility in India (launched Sept 2024) exemplifies expansion into smallholder farmer participation.

The biochar market is experiencing extreme supply constraints. As of Q2 2025, 89% of 2025 credits are already committed up from 62% in March 2025. Even 2026 credits are 40% locked into offtake agreements, with buyers racing to secure supply over a year in advance. This scarcity is driving 8% quarter-over-quarter price increases and 10–20% premiums for operational projects with proven delivery track records.

| Year | Price/Tonne (USD) | Change |

|---|---|---|

| 2023 | $131 | Baseline |

| 2024 | $145 (est.) | +11% |

| 2025 (H1) | $164 | +25% YoY |

The 25% price increase from 2023 to 2025 reflects growing demand and constrained supply. Standards like Puro.earth command the highest prices due to methodological rigor, while Verra credits trade at a discount. Gold Standard biochar credits often trade 10–20% higher than Verra due to integrated SDG impact assessments, appealing to ESG-focused buyers.

Explore the science behind biochar, its role in regenerative agriculture, potential carbon-market benefits, and how it can contribute to more sustainable and resilient food systems.

Read the full blog on Biochar for Carbon Removal →

The integrity of biochar carbon credits depends entirely on the standard and methodology used. Independent verification by accredited Validation & Verification Bodies (VVBs) ensures that claims are scientifically sound, methodologically rigorous, and free from double-counting.

On February 3, 2026, the European Commission formally adopted biochar carbon removal under the CRCF Regulation, officially categorizing BCR as a permanent carbon removal methodology eligible for compliance-ready, high-integrity credits.

| Standard | Rigor | Cost/Timeline | Focus Area |

|---|---|---|---|

| Puro.earth | Highest | $50k–$100k; 12–15 months | Permanence & engineered removal |

| Verra VM0044 | High | $30k–$70k; 12–18 months | Lifecycle accounting & global scale |

| Gold Standard | High | $50k–$100k; 12–15 months | SDG alignment & social impact |

| CSI | Medium | $15k–$30k; 6–12 months | Artisanal & smallholder projects |

Learn how leading carbon standards evaluate projects, the differences between major certification frameworks, and what organizations should consider when assessing carbon credits for sustainability and net-zero strategies.

Read the full blog on Carbon Offset Standards →

MRV is the backbone of biochar carbon credit credibility. It ensures that credits represent real, measurable, and permanent carbon removal not greenwashing.

| Phase | What It Means | Key Actors | Timeline |

|---|---|---|---|

| Monitoring | Continuous collection of project data: feedstock inputs, biochar yields, energy consumption, soil application records. Digital MRV platforms increasingly used. | Project operators, IoT sensors, ERP systems | Ongoing |

| Reporting | Compilation of monitoring data into formal monitoring reports submitted to standard body. Includes emissions calculations, permanence claims, and co-product allocations. | Project developers, dMRV platforms | Annual or per-batch |

| Verification | Independent third-party auditor (Validation & Verification Body) reviews all data and confirms methodology compliance. Issues verification statement. | Accredited VVB (appointed by standard body) | 3–6 months after reporting |

| Issuance | Standard body issues tradeable carbon credits (VCUs, CORCs) to project account in public registry. 1 credit = 1 tonne CO₂e. | Standard body (Verra, Puro.earth, etc.) | Upon approval |

Digital MRV systems (dMRV) are increasingly adopted, integrating IoT sensors, ERP systems, and automated data collection from suppliers. Platforms like Carbonfuture provide standardized digital infrastructure supporting verification across multiple standards (Puro.earth, Verra, Isometric, CSI, CAR).

Discover how dMRV helps automate data collection, improve transparency, reduce reporting burdens, and create audit-ready sustainability records across complex supply chains.

Read the full blog on dMRV (Digital Measurement, Reporting & Verification) →

Credible methodologies from standards like Puro.earth, Verra VM0044, Isometric, and CAR include explicit guidance on co-product allocation and stack emissions monitoring. Projects unable to provide third-party verification of these metrics are not investment-grade.

Current Market Price (H1 2025): $164/tonne

This represents a 25% increase from $131/tonne in 2023, driven by supply scarcity, growing corporate demand, and improving market integrity.

Experts project biochar credit valuations to reach $250–$300/tonne by 2030 as supply expands and standardization deepens. However, price stability remains dependent on broadening the buyer base beyond the current oligopoly of Fortune 500 companies and expanding into mid-market and SME segments.

Learn how voluntary carbon markets work, the key stakeholders involved, evolving integrity standards, and what businesses need to evaluate before investing in carbon-credit programs.

Read the full blog on Voluntary Carbon Markets →

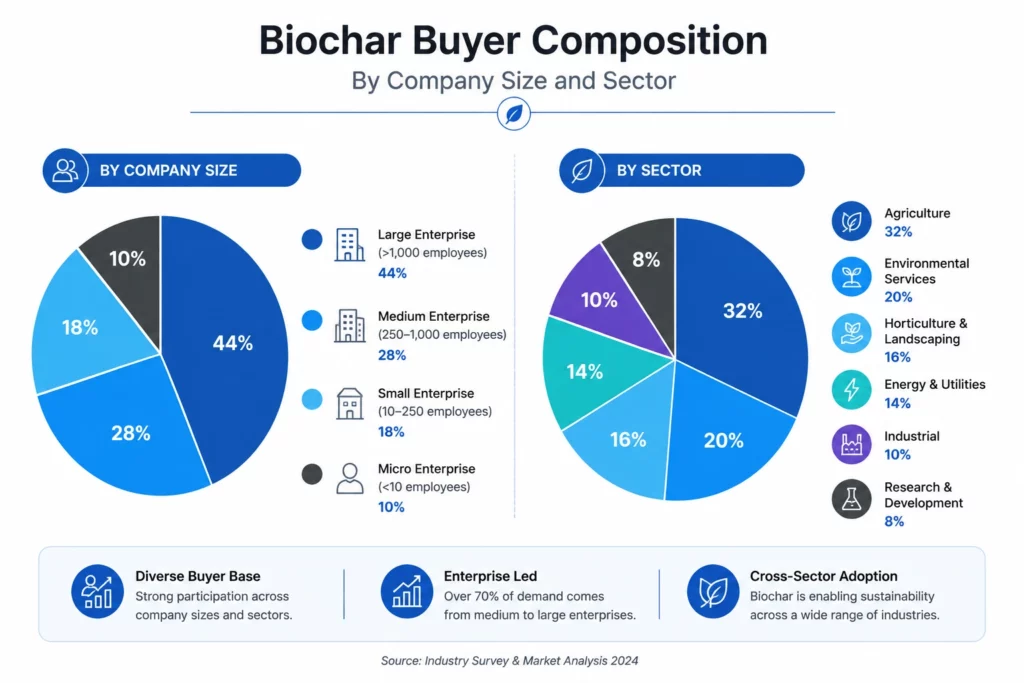

Despite rapid market growth, biochar credit purchases remain highly concentrated. A handful of Fortune 500 companies account for the majority of procurement:

| Company | Sector | Contracted Volume | Status |

|---|---|---|---|

| Microsoft | Technology | 1.24M tonnes (Q2 2025) | Active major buyer |

| Technology | 500k+ tonnes (est.) | Active buyer | |

| JPMorgan Chase | Financial Services | 250k+ tonnes (est.) | Active buyer |

| Swiss Re | Insurance | 200k+ tonnes (est.) | Active buyer |

| BCG | Professional Services | 100k+ tonnes (est.) | Active buyer |

This concentration creates a paradox: strong demand that drives price increases, but fragile market structure susceptible to disruption if even one major buyer reduces commitments.

Market developers are actively working to expand beyond the oligopoly:

For corporations and asset managers considering biochar carbon credit investments, several critical challenges and decision factors warrant attention:

TraceX dMRV (Digital Measurement, Reporting, and Verification) helps biochar projects move from manual record-keeping to a structured, audit-ready system for carbon accounting and project verification.

By creating a transparent, traceable, and verifiable digital audit trail, TraceX dMRV helps biochar developers improve project credibility, simplify carbon-credit issuance processes, and demonstrate measurable climate impact with greater confidence.

| Attribute | Biochar | Nature-Based | Direct Air Capture |

|---|---|---|---|

| Price ($/tonne) | $164 | $50–$200 | $200–$600 |

| Permanence | 100+ years | 20–100 years (risk) | Permanent (geological) |

| Co-benefits | Soil health, crop yield, farmer income | Biodiversity, water, ecosystem | Minimal |

| Scalability | High (abundant biomass) | Limited (land constraint) | Limited (capital, energy) |

| Time to Impact | 1–2 years | 10–20 years | Immediate |

Biochar’s advantage lies in permanence, cost, and scalability. Unlike nature-based offsets (reforestation, REDD+), biochar carbon is engineered to be stable for 100+ years. At $164/tonne, biochar is cheaper than direct air capture ($200–$600/tonne) while offering faster deployment than afforestation (which requires 10–20 years to mature). However, biochar depends on consistent biomass supply and operates at smaller scale than forest carbon programs.

Explore how Nature-Based Solutions work, their role in climate mitigation and adaptation, and why businesses, governments, and investors are increasingly integrating nature into their sustainability strategies.

Read the full blog on Nature-Based Solutions →

| Step | Action Items |

|---|---|

| 1 | Define Procurement Goals Determine budget allocation for biochar (recommend 5–15% of total carbon removal budget). Set permanence requirements (100+ years preferred). Identify ESG/SDG priorities (e.g., farmer income, biodiversity co-benefits). |

| 2 | Select Verification Standard Choose standard based on goals: Puro.earth for highest rigor, Verra VM0044 for scale, Gold Standard for SDG alignment, CSI for smallholder projects. Budget $30k– $100k for certification costs and 12–18 month timeline. |

| 3 | Verify Delivery Track Record Use public registries (Puro.earth, Verra, Isometric, CAR) to check project history: How many credits issued? How many retired? Delivery delays? Prioritize projects with 2+ years of proven deliveries and 70%+ delivery-to-contracted ratio. |

| 4 | Demand MRV Documentation Request third-party verified Lifecycle Assessment (LCA), feedstock traceability docs, pyrolysis monitoring data, H/Corg stability testing, and emissions accounting. If project uses digital MRV, verify platform credibility and transparency. |

| 5 | Diversify Portfolio Spread purchases across 5–10 projects, multiple standards (Puro/Verra/Gold Standard), geographies (North America, Europe, Emerging Markets), and project scales (industrial vs. smallholder). Limits concentration and execution risk. |

| 6 | Structure Offtake Agreements Negotiate 3–5 year contracts locking in pricing and delivery timelines. Include performance penalties for delays. Specify permanence insurance or buffer accounts. Consider price escalation clauses to share in future price upside as market matures. |

| 7 | Monitor & Report Track portfolio performance against net-zero targets. Monitor for delivery delays, price volatility, and standard changes. Publish transparent ESG reporting on carbon removal, permanence, and co-benefits. Engage with market participants on buyer-base diversification. |

By following this framework, buyers can navigate the complexities of biochar credit procurement while managing risk and maximizing impact integrity.

Biochar carbon credits represent a compelling climate solution for corporates and asset managers seeking durable, cost-effective carbon removal. The market is growing at 27.4% CAGR, driven by Fortune 500 demand and emerging compliance frameworks like the EU CRCF.

However, extreme supply scarcity, buyer concentration, and methodological variability create meaningful risks. Successful biochar procurement requires careful standard selection, rigorous MRV due diligence, and diversified project portfolio strategy.

For buyers comfortable with emerging-market risk and able to lock in multi-year offtake agreements, biochar offers a rare opportunity: engineered carbon removal with agricultural co-benefits, proven third-party verification, and institutional-grade permanence. For conservative buyers seeking maximum certainty, delayed purchasing until supply normalizes (2027+) and buyer base broadens may be prudent.

The next 18 months will be decisive for biochar market trajectory. Early adopters with strong due diligence discipline will position themselves advantageously as the market matures.

Biochar carbon credits are carbon removal credits generated when biomass is converted into stable biochar through pyrolysis and applied to soils or other approved end uses. Because biochar can store carbon for hundreds to thousands of years, the resulting carbon sequestration can be quantified, verified, and issued as tradable carbon credits under approved methodologies.

Biochar carbon credits are typically purchased by:

Demand is growing because biochar credits are often viewed as durable carbon removals with measurable climate benefits and relatively low reversal risk compared to some nature-based projects.

Biochar projects must undergo rigorous monitoring, reporting, and verification processes before credits are issued.

Verification generally includes:

Many projects also use digital MRV (dMRV) systems to improve data quality, transparency, and audit readiness.

Several factors affect biochar credit pricing, including:

Projects with strong traceability and robust verification frameworks often command premium pricing.

Traceability helps demonstrate that feedstocks are sourced responsibly, production processes are properly documented, and carbon-removal claims can be verified.

Strong traceability systems support:

As voluntary carbon markets mature, transparent data, digital MRV systems, and end-to-end traceability are becoming increasingly important for project credibility and long-term market acceptance.